This blog post was originally posted on Austin Technology Council's weekend update on August 19, 2016.

We can all agree that efficient communication is the most critical bridge between private equity firms and their clients. Since regulatory requirements are constantly changing, it can be hard for .

Everyone understands that cash management is a top priority when trouble hits, but the scale and intensity of the fallout from COVID-19 leaves little room for a sluggish or lax response. Here are .

In the wake of COVID-19, businesses must remain agile and disciplined, which requires making finance teams fully operational out of the office. Consero’s President Bill Klein offers a few key tips on .

Business process outsourcing (BPO) has seen a considerable increase in market demand during the last few years. According to research, the BPO industry is expected to reach USD 405.6 billion by 2027. .

To strengthen and continuously improve their private equity portfolio, private equity firms need to go beyond the traditional role of being a mere provider of capital. With ROI always in mind, due .

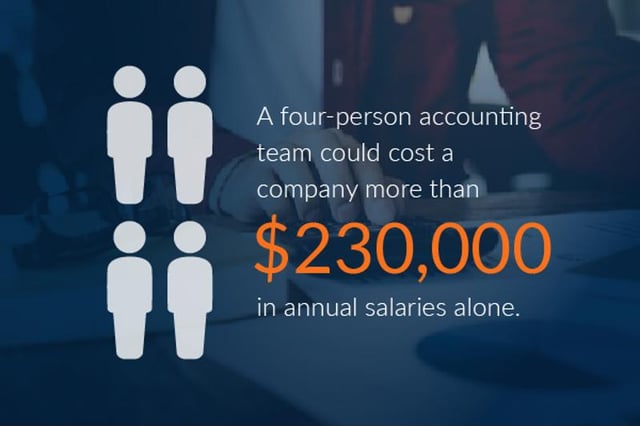

To achieve the level of productivity and efficiency that allows a private equity firm to maintain financial stability and ability to scale, many PE firms have decided to outsource accounting for .

If you want to grow your business as a private equity firm, lowering operational costs and maximizing ROI across all portfolio companies should be your starting points. However, as your PE portfolio .

Private equity firms embarking on buy and build strategies should have a plan to effectively scale the finance function, says Consero Global’s President, Bill Klein.

The term “digital transformation” has been thrown around a lot, particularly in the past decade. But what is it? Is it a trend or the latest buzzword? Or is it the direction that all businesses must .

With artificial intelligence (AI), robotic process automation (RPA) and smart analytics powering the future of finance and accounting, manual bookkeeping and spreadsheet-based solutions will soon be .